The balance sheet isn’t what it used to be

Today, the relative importance of tangible assets compared to intangibles has completely flip-flopped from what it was 40 years ago. Intangibles now account for over 80% of the average company’s market value. Intangibles like brand names, customer lists, R&D spending, and patents have become increasingly more important to how we value companies.

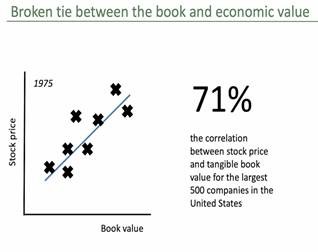

For companies in the S&P 500 today, the correlation between stock price and tangible book value has become quite small, just 14%. This is a very big change from 25 years ago when that correlation was 71%.

The expensive getting more expensive

Only once before have the most expensive stocks been relatively more expensive and that was during the internet bubble.

Small-cap balance sheets looking riskier than large-cap

China scrambles to stem manufacturing exodus

Many companies, alarmed by the prospect of a prolonged trade conflict, are hedging their bets. While looking for alternative production sites for U.S.-bound goods, many will keep factories operating in China for the domestic Chinese market. Thus, many manufacturers will be forced to set up dual supply chains: one for China and one for other markets, raising their costs and denting profits.

The trade dispute is beginning to show up in flows of goods and capital. In the first five months of the year, exports from China to the U.S. fell 12% on the year in value terms, while those from India, Vietnam and Taiwan logged double-digit gains.

Much of the shift is to Southeast Asia, especially Vietnam, which is becoming home to many manufacturers of electrical and electronic equipment.

Today, the relative importance of tangible assets compared to intangibles has completely flip-flopped from what it was 40 years ago. Intangibles now account for over 80% of the average company’s market value. Intangibles like brand names, customer lists, R&D spending, and patents have become increasingly more important to how we value companies.

For companies in the S&P 500 today, the correlation between stock price and tangible book value has become quite small, just 14%. This is a very big change from 25 years ago when that correlation was 71%.

The expensive getting more expensive

Only once before have the most expensive stocks been relatively more expensive and that was during the internet bubble.

Source: Exane BNP Paribas estimates

With four generations of retail investors now involved in financial markets, attitudes and approaches to investing are beginning to diverge. How did different generations of investors react to recent bouts of volatility in the market?

China scrambles to stem manufacturing exodus

Many companies, alarmed by the prospect of a prolonged trade conflict, are hedging their bets. While looking for alternative production sites for U.S.-bound goods, many will keep factories operating in China for the domestic Chinese market. Thus, many manufacturers will be forced to set up dual supply chains: one for China and one for other markets, raising their costs and denting profits.

The trade dispute is beginning to show up in flows of goods and capital. In the first five months of the year, exports from China to the U.S. fell 12% on the year in value terms, while those from India, Vietnam and Taiwan logged double-digit gains.

Much of the shift is to Southeast Asia, especially Vietnam, which is becoming home to many manufacturers of electrical and electronic equipment.