2020 Q1 EdgePoint commentary

In this quarter’s equity and fixed-income commentaries, we address the gravity of the responsibility you have entrusted us with. We know that you have a similar responsibility to your own clients. For the first time, we have also recorded a podcast of the commentaries.

Equity commentary: We understand the gravity of our responsibility to you – 1st quarter, 2020

Fixed-income commentary: Glass half full – 1st quarter, 2020

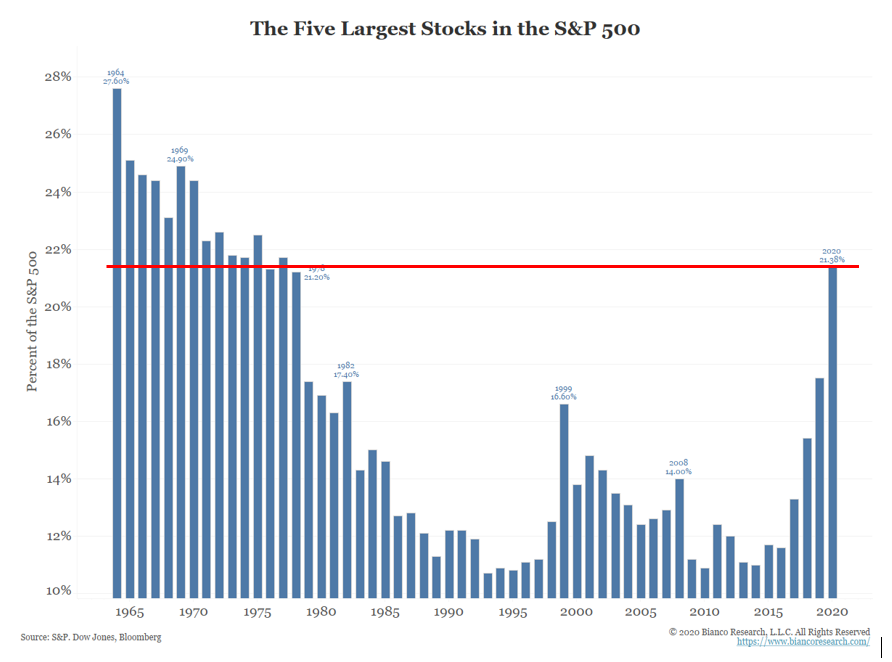

Which way now?

In the last six weeks the markets have seen the best of times and the worst of times:

- From February 19 to March 23, the U.S. stock market saw the quickest meltdown in history, for a loss of 33.9% on the S&P 500. Then its 17.5% gain from Tuesday through Thursday of last week made for the best three-day stretch since the 1930s.

- Of the 21 trading days between February 27 and March 27, a total of 18 days saw moves in the S&P 500 of more than 2%: eleven down and seven up. They included the biggest daily percentage gain since 1933 and the second-biggest percentage loss since 1940 (exceeded only by Black Monday in 1987).

- From March 9 through March 20, issuing a new investment-grade bond seemed inconceivable. Then, as our trader Justin Quaglia points out, last week’s news of the government’s rescue package enabled 49 companies to issue $107 billion of IG bonds. That made it the biggest week for issuance on record; In fact, there was more issuance last week than in nine of the 12 months in 2019.

- Finally, on March 26, Justin wrote, “It’s hard to believe I used the words ‘panic’ and ‘FOMO’ within two weeks of each other.”

Looking at the above, it’s important to note the degree to which people (and thus markets) seem to think long-term phenomena can change in the short run.

A chart that may prove useful:

On average the market bottoms 5 months before the recessions ends, and rallies 26% before the recession is officially over.

The Craziest Month in Stock Market History

But enough of the numbers and charts. The thing that made March 2020 especially insane for most investors was the constant news coverage and speed at which everything was happening.

The entire month was an onslaught of information, fear, and uncertainty. And to top it all off, we spent most of this month physically separated from each other, sitting within the same 4 walls every day.

So no matter how crazy this month was for you, the most important thing to remember is that…it ended.

Market volatility may not go away anytime soon, but the important thing to remember is that investing isn’t about a single decision, but a collection of decisions over a lifetime. The biggest important thing is to make sure that you live to invest another day. A lot of the very basic stupid mistakes are the most important things to avoid.

Family's lockdown adaptation of Les Misérables song goes viral

A family from Kent who shared a video of their living room performance of a lockdown-themed adaptation of a Les Misérables song has become a sensation online. Ben and Danielle Marsh and their four children changed the lyrics of One Day More to reflect common complaints during the COVID-19 lockdown. They say the video, which has gone viral, was intended to give friends and family a laugh during this stressful time.

How to stay creative and keep your family sane during the lockdown

British art and textiles teacher Andria Zafirakou won the 2018 Global Teacher Prize and has two teenage daughters. Here she gives some practical tips – from giving your children time to transition to homeschooling, to creative ideas – for navigating staying at home together. Parents can encourage creativity. Here are just a couple from the list.

- Asking questions: Creativity is all about questioning: How can I? Why should it? What would happen if? How can I make this, or how can I change this? It’s about making sure that children are always being asked those questions.

- Keeping everything: Do not chuck anything away. Keep a bag with all the egg boxes and toilet rolls in a corner, because that’s going to be a mine of incredible craft-making materials.

- Giving them time: The beauty is that the parents are in control of the time, for once. So you can give your child two hours to get on with a wonderful creative task, and they wouldn’t have that in school.

- Thinking outside the paintbox: Creativity is not just about arts and crafts, it’s also about the kitchen. What kind of lunch can they make for you while you’re working?