U.S. mortgage debt hits a new record

U.S. mortgage debt reached a new record in the second quarter, exceeding its 2008 peak. The steep drop in mortgage rates boosted borrowers’ incentive to take out a mortgage or refinance. Alongside higher home prices, a factor behind rising mortgage debt balances is homeowners tapping into home equity for cash when they refinance. Still, the household debt picture is different in 2019. Despite the higher debt levels, Americans appear to be keeping up with their payments.

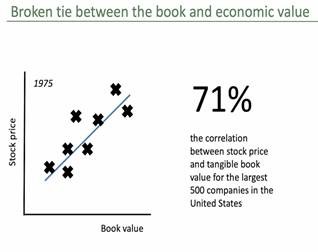

EdgePoint bond desk: Four more rate cuts might be excessive

Core prices rose 2.2% versus a year earlier in July, the largest increase since December. Even this increase counts as tame and suggests that the Fed's preferred measure of core prices may remain below the 2% inflation target. Still, after the two largest back-to-back monthly increases in core prices since 2006, when the Fed was on the inflation-fighting warpath, it is harder to get worked up about “too low” inflation. Especially with the unemployment rate at 3.7%.

It's never been cheaper to borrow in Denmark

Banks in Denmark are now effectively paying qualified homebuyers who take out a 10-year fixed-rate mortgage. Jyske Bank, the third-largest bank in Denmark, will now lend to prospective homebuyers at an interest rate of -0.5%.

Risk in investing

Risk is the four-letter word of investing, but it is poorly understood. Consider, for example, the two different investments in the accompanying table: Investment A and Investment B.

Which investment would you prefer? A or B?

Everyone would prefer investment A. After all, you end up with more money after three years. But, which investment is riskier? According to investment orthodoxy, Investment A is riskier! Why? Because it has a higher standard deviation (or volatility of returns) at 23.6% than Investment B at 0%. Doesn’t that strike you as odd? In investing, if you don’t want volatility, then you have to accept that you won’t have much upside potential.

We asked Sandro, the most passionate movie buff at EdgePoint, for his top 10 movie picks of all time. After agonizing for days over this list, this was his response:

Films have had a profound influence on shaping the man I am. In fact, great films have the power not only to entertain but more importantly to transform the way we see the world. Truly great films, like a great vintage wine, get better with age. Each subsequent viewing reveals new pleasures and they become more socially and culturally relevant.

Ok. That’s enough with my ramblings. Keep in mind that if you asked me next week, it might be a completely different list. I didn’t even include a foreign film. I love foreign films!

Sandro’s Top 10 of All Time… more specifically on August 13, 2019

Citizen Kane (1941) - Welles

Casablanca (1942) - Curtiz

Vertigo (1958) – Hitchcock

The Good, the Bad & the Ugly (1966) - Leone

The Godfather (1972) – Coppola

Annie Hall (1977) - Allen

Goodfellas (1990) – Scorsese

Pulp Fiction (1994) – Tarantino

Boogie Nights (1997) – Anderson

The Social Network (2010) - Fincher

U.S. mortgage debt reached a new record in the second quarter, exceeding its 2008 peak. The steep drop in mortgage rates boosted borrowers’ incentive to take out a mortgage or refinance. Alongside higher home prices, a factor behind rising mortgage debt balances is homeowners tapping into home equity for cash when they refinance. Still, the household debt picture is different in 2019. Despite the higher debt levels, Americans appear to be keeping up with their payments.

EdgePoint bond desk: Four more rate cuts might be excessive

Core prices rose 2.2% versus a year earlier in July, the largest increase since December. Even this increase counts as tame and suggests that the Fed's preferred measure of core prices may remain below the 2% inflation target. Still, after the two largest back-to-back monthly increases in core prices since 2006, when the Fed was on the inflation-fighting warpath, it is harder to get worked up about “too low” inflation. Especially with the unemployment rate at 3.7%.

It's never been cheaper to borrow in Denmark

Banks in Denmark are now effectively paying qualified homebuyers who take out a 10-year fixed-rate mortgage. Jyske Bank, the third-largest bank in Denmark, will now lend to prospective homebuyers at an interest rate of -0.5%.

Risk is the four-letter word of investing, but it is poorly understood. Consider, for example, the two different investments in the accompanying table: Investment A and Investment B.

Which investment would you prefer? A or B?

Everyone would prefer investment A. After all, you end up with more money after three years. But, which investment is riskier? According to investment orthodoxy, Investment A is riskier! Why? Because it has a higher standard deviation (or volatility of returns) at 23.6% than Investment B at 0%. Doesn’t that strike you as odd? In investing, if you don’t want volatility, then you have to accept that you won’t have much upside potential.

We asked Sandro, the most passionate movie buff at EdgePoint, for his top 10 movie picks of all time. After agonizing for days over this list, this was his response:

Films have had a profound influence on shaping the man I am. In fact, great films have the power not only to entertain but more importantly to transform the way we see the world. Truly great films, like a great vintage wine, get better with age. Each subsequent viewing reveals new pleasures and they become more socially and culturally relevant.

Ok. That’s enough with my ramblings. Keep in mind that if you asked me next week, it might be a completely different list. I didn’t even include a foreign film. I love foreign films!

Sandro’s Top 10 of All Time… more specifically on August 13, 2019

Citizen Kane (1941) - Welles

Casablanca (1942) - Curtiz

Vertigo (1958) – Hitchcock

The Good, the Bad & the Ugly (1966) - Leone

The Godfather (1972) – Coppola

Annie Hall (1977) - Allen

Goodfellas (1990) – Scorsese

Pulp Fiction (1994) – Tarantino

Boogie Nights (1997) – Anderson

The Social Network (2010) - Fincher