Cymbria’s 2023 annual report

Cymbria’s most-recent annual report is now available for your reading pleasure. You can find insights on how Cymbria navigated the last year and updates on our largest holding, EdgePoint Wealth Management.

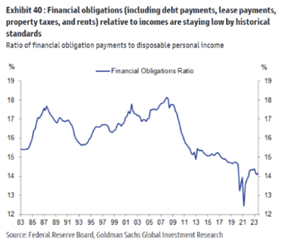

This week in charts

Manufacturing

Small-caps

Automotive

Energy

Housing

US small-caps suffer worst run against larger stocks in more than 20 years

US small-cap stocks are suffering their worst run of performance relative to large companies in more than 20 years, highlighting the extent to which investors have chased megacap technology stocks while smaller groups are weighed down by high interest rates.

The Russell 2000 index has risen 24 per cent since the beginning of 2020, lagging the S&P 500’s more than 60 per cent gain over the same period. The gap in performance upends a long-term historical norm in which fast-growing small-caps have tended to deliver punchier returns for investors who can stomach the higher volatility.

The unusually wide spread between the two closely watched indices has opened up in recent years as small-cap stocks with relatively weak balance sheets and modest pricing power have been especially hurt by high inflation and a steep rise in borrowing costs, according to analysts, putting off many investors.

The S&P has climbed steadily since early November, with strong earnings and investor excitement about the artificial intelligence boom driving huge gains for the likes of Nvidia and Meta.

In contrast, the small-cap rally that gathered pace in the final months of 2023 has petered out this year, expanding an already wide gap in performance. Utilities and telecoms groups such as broadband company Gogo, Vertex Energy and Middlesex Water are among stocks that have been hit.

Aside from a brief period of outperformance in 2020 during the early stages of the coronavirus pandemic, small-cap stocks have lagged their larger peers since 2016.

In the 2000s, before global interest rates sank to close to zero following the financial crisis, thinly-traded and under-analysed stocks had on average outperformed the biggest companies. Analysts attribute this pattern to a combination of market inefficiency and the explosive growth potential of tomorrow’s market leaders.

“When you get small-caps right, you’re not right by 20 per cent more than the Street, your earnings and revenue estimates could be double where the consensus is . . . That leads to a more significant price gain,” said Tuorto, whose portfolio is dominated by stocks including Shake Shack and Wingstop, as well as retailers.

Although there are signs that the equity market rally is beginning to broaden out beyond the biggest tech stocks, stubborn inflation and a resilient jobs market have recently contributed to an acceptance among traders that interest rates may stay higher for longer than they had anticipated just a few months ago.

In a worst-case scenario where the Federal Reserve is forced to keep rates on hold for months to come or even raise them, smaller companies are likely to be the hardest hit. Roughly 40 per cent of debt on Russell 2000 balance sheets is short-term or floating rate, compared with about 9 per cent for S&P companies.

Fourth-quarter earnings for Russell 2000 companies, about 30 per cent of which are unprofitable, fell 17.6 per cent year-on-year, according to LSEG data. Earnings for S&P companies, in contrast, rose by about 4 per cent, although a large portion of the gain was driven by the so-called Magnificent Seven tech stocks.

However, barring a recession, small-cap profits are expected to improve as rates start to come down. Fed chair Jay Powell last week left rates unchanged and signalled a preference to cut by three-quarters of a percentage point this year, pushing the Russell 2000 up by a percentage point more than the S&P on the day.

Flawed Valuations Threaten $1.7 Trillion Private Credit Boom

Colm Kelleher whipped up a storm at the end of last year when the UBS Group AG chairman warned of a dangerous bubble in private credit. As investors dive headfirst into this booming asset class, the more urgent question for regulators is how anybody could even know for sure what it’s really worth.

The meteoric rise of private credit funds has been powered by a simple pitch to the insurers and pensions who manage people’s money over decades: Invest in our loans and avoid the price gyrations of rival types of corporate finance. The loans will trade so rarely — in many cases, never — that their value will stay steady, letting backers enjoy bountiful and stress-free returns. This irresistible proposal has transformed a Wall Street backwater into a $1.7 trillion market.

Now, though, cracks in that edifice are starting to appear.

Central bankers’ rapid-fire rate hikes over the past two years have strained the finances of corporate borrowers, making it hard for many of them to keep up with interest payments. Suddenly, a prime virtue of private credit — letting these funds decide themselves what their loans are worth rather than exposing them to public markets — is looking like one of its greatest potential flaws.

Data compiled by Bloomberg and fixed-income specialist Solve, as well as conversations with dozens of market participants, highlight how some private-fund managers have barely budged on where they “mark” certain loans even as rivals who own the same debt have slashed its value.

In one loan to Magenta Buyer, the issuing vehicle of a cybersecurity company, the highest mark from a private lender at the end of September was 79 cents, showing how much it would expect to recoup for each dollar lent. The lowest mark was 46 cents, deep in distressed territory. HDT, an aerospace supplier, was valued on the same date between 85 cents and 49 cents.

This lack of clarity on what an asset’s worth is a regular complaint in private markets, and that’s spooking regulators. While nobody cared too much when central bank interest rates were close to zero, today financial watchdogs are fretting that the absence of consensus may be hiding more loans in trouble.

“In private markets, because no one knows the true valuation there’s a tendency to leak information into prices slowly,” says Peter Hecht, managing director at US investment firm AQR Capital Management. “It dampens volatility, giving this false perception of low risk.”

The private-lending funds and companies mentioned in this story all declined to comment, or didn’t respond to requests for a comment.

Code of Silence?

Private credit was embraced at first for shifting risky company loans away from systemically important Wall Street banks and into specialist firms, but the ardor’s cooling in some quarters. Regulators are doubly nervous because of the economy’s febrile state. These funds charge interest pegged to base rates, which has handed them bumper profits — and made their borrowers vulnerable.

“As interest rates have risen, so has the riskiness of borrowers,” Lee Foulger, the Bank of England’s director of financial stability, strategy and risk, said in a recent speech. “Lagged or opaque valuations could increase the chance of an abrupt reassessment of risks or to sharp and correlated falls in value, particularly if further shocks materialize.”

Values are especially cloudy outside the US, because of poor transparency. And it’s the same for loans made by funds that don’t publish quarterly updates or where there’s a single lender with no one to judge them against.

Tyler Gellasch, head of the Healthy Markets Association, a trade group that includes pension funds and other asset managers, says policymakers have been caught napping. “This is simply a regulatory failure,” says Gellasch, who helped draft part of the Dodd-Frank Wall Street reforms after the financial crisis. “If private funds had to comply with the same fair value rules as mutual funds, investors could have a lot more confidence.”

The Securities and Exchange Commission has nevertheless begun to pay closer attention, rushing in rules to force private-fund advisers to allow external audits as an “important check” on asset values.

Red Flags

The thinly traded nature of this market may make it nigh-on impossible for most outsiders to get a clear picture of what these assets are worth, but red flags are easier to spot. Take the recent spike in so-called “payment in kind” (or PIK) deals, where a company chooses to defer interest payments to its direct lender and promises to make up for it in its final loan settlement.

An equally perplexing sign is the number of private funds who own publicly traded loans, and still value them much more highly than where the same loan is quoted in the public market.

In a recent example, Carlyle Group Inc.’s direct-lending arm helped provide a “second lien” junior loan to a US lawn-treatment specialist, TruGreen, marking the debt at 95 cents on the dollar in its filing at the end of September. The debt, which is publicly traded, was priced at about 70 cents by a mutual fund at the time. Most private credit portfolios “remain above their public market peers,” the BoE’s Foulger noted in his speech on “nonbank” lenders.

And it’s not just the comparison with public prices that is sometimes out of whack. As with Magenta Buyer and HDT there are eye-catching cases of separate private credit firms seeing the same debt very differently. Thrasio is an e-commerce business whose loan valuations have been almost as varied as the panoply of product brands that it sells on Amazon, which runs from insect traps and pillows to cocktail shakers and radio-controlled monster trucks.

As the company has struggled lately, its lenders have been divided on its prospects. Bain Capital and Oaktree Capital Management priced its loans at 65 cents and 79 cents respectively at the close of September. Two BlackRock Inc. funds didn’t even agree: One valuing its loan at 71 cents, the other at 75 cents. Monroe Capital was chief optimist, marking the debt at 84 cents. Goldman Sachs Group Inc.’s asset management arm had it at 59 cents.

The Wall Street bank seems to have made the shrewder call. Thrasio filed for Chapter 11 on Wednesday as part of a debt restructuring deal and one of its public loans is quoted well below 50 cents, according to market participants. Oaktree lowered its mark to 60 cents in December.

“Dispersions widen when a company is falling into distress as well as when a lot of funds are marking the same asset,” says Bloomberg Intelligence analyst Ethan Kaye. “When a company is either stressed or distressed, it becomes less certain as to what future cash flows might look like.”

In an analysis of Pitchbook data from the end of September, Kaye found that in one in 10 cases where the same debt was held by two or more funds, the price gap was at least 3%. When three of four funds own the same loan, something that’s common in this industry, the differences get starker still.

Distressed companies do throw up some especially surprising values. Progrexion, a credit-services provider, filed for bankruptcy in June after losing a long-running lawsuit against the US Consumer Financial Protection Bureau. Its bankruptcy court filing estimated that creditors at the front of the queue would get back 89% of their money. Later that month its New York-based lender Prospect Capital Corp. marked the senior debt at 100 cents.

In data pulled together by Solve on the widest gaps between how a lender marks its loans versus other parties’ valuations, Prospect’s name appears more regularly than most. BI finds that smaller firms in general appear to mark their loans more aggressively.

Private Fans

For private credit’s many champions, the criticism’s overblown. Fund managers argue that they don’t need to be as brutal on marking down prices because direct loans usually involve only one or a handful of lenders, giving them much more control during tough times. In their eyes, the beauty of this asset class is that they don’t have to jump every time there’s a bump in the road.

Some investors point as well to the shortcomings of the leveraged-loan market, private credit’s biggest rival as a source of corporate finance, where Wall Street banks gather large syndicates of mainstream lenders to fund companies.

“There are a lot of technicals that influence the broadly syndicated loan market, like sales encouraged by ratings downgrades or investors getting out of certain sectors,” says Karen Simeone, managing director at private markets investor HarbourVest Partners. “You don't get this in private credit and so I do think it makes sense that these valuations are less volatile.”

Direct lenders also use far less borrowed money than bank rivals, giving regulators some comfort that any market blowup could be contained. They typically lock in cash they get from investors for much longer periods than banks, and they don’t tap customer deposits to pay for their risky lending. They tend to have better creditor protections, too.

Third-party advisers such as Houlihan Lokey and Lincoln International are increasingly assessing loan marks, adding scrutiny, though it’s paid for by the funds and is no panacea. “We don't always get unfettered access to credits,” says Timothy Kang, co-lead of Houlihan’s private credit valuation practice. “Some managers have access to more information than others.”

In the US, direct lenders often set up as publicly listed “business development companies,” requiring them to update their investors every quarter. BDCs do give better visibility on their loan prices but their fund managers are paid according to the portfolio’s worth so there’s an incentive to mark debt high.

This week’s fun finds

These pizza-covered watches are a cheesy April Fools joke made real

Here’s a story of what happens when an April Fools day joke becomes reality – and why a startup British watchmaker just revealed a new collection with dials inspired by pizza toppings.

To understand how such a watch came to be, we need to wind the hands back to 1 April 2023, when Studio Underd0g published a video featuring Richard Benc and Andrew McUtchen – founders of Studio Underd0g and Time + Tide, respectively – teasing a new watch collection inspired by pizza.

Within a few hours, the Studio Underd0g website had received 20,000 visitors and 800 pizza enthusiasts had expressed interest in purchasing the quirky watch. Fast-forward to the present day, and the Pizza-Party collection is real.

One watch is called the Pepper0ni, with a cheesy dial featuring meat, olives and mushrooms, and the other watch is called Hawaiian, with the iconic (not to mention controversial) toppings of ham and pineapple. Underd0g says of the Hawaiian: “We have no doubt that the Pepper0ni may have ruffled a few feathers in Switzerland by making a mockery of their beloved industry, so why not double down and wind up some Italians too?”.

Priced at £550, both watches surround their dial with a crispy crust – sorry, I mean a beige tachymeter – and both feature a 38.5mm stainless steel case housing a Seagull ST-1901 automatic chronograph movement, visible through the exhibition case back. The watches are both water resistant to 50 metres and they have 50 hours of power reserve.

Finally, and just to make them even more quirky, the watches cannot be bought online. They can’t even be bought from a shop or a boutique. Instead, they are only available to purchase directly from Richard Benc or Andrew McUtchen in person. So they’re hand-delivered, just like a takeaway pizza. No word on whether the watches will be presented on a sheet of greaseproof paper in a cardboard box, but I wouldn’t bet against it!

The Studio Underd0g website has details of where to find the watches through 2024. The first opportunity was in Australia on 19 January (sorry, we’re a bit late to the pizza party on this one), but the next is in Leeds on 8 February, followed by London on 9 March, San Francisco in May, Chicago in July, Geneva in September and New York in October. Further opportunities will take place in Manchester, Oxford, Birmingham, Toronto and Dubai, but the dates for these haven’t yet been announced.

{kind=link}