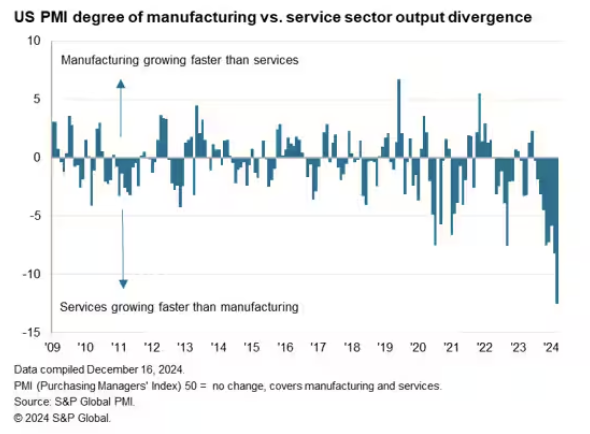

This week in charts

S&P 500 outperformance

Magnificent 7

2025 interest rate cuts

Foreign exchange reserves

Imports from China

Tariffs

Household balance sheets

U.S. stock & bond correlation

Defaults on leveraged loans soar to highest in 4 years

US companies are defaulting on junk loans at the fastest rate in four years, as they struggle to refinance a wave of cheap borrowing that followed the Covid pandemic.

Defaults in the global leveraged loan market — the bulk of which is in the US — picked up to 7.2 per cent in the 12 months to October, as high interest rates took their toll on heavily indebted businesses, according to a report from Moody’s. That is the highest rate since the end of 2020.

The rise in companies struggling to repay loans contrasts with a much more modest rise in defaults in the high-yield bond market, highlighting how many of the riskier borrowers in corporate America have gravitated towards the fast-growing loan market.

Because leveraged loans — high yield bank loans that have been sold on to other investors — have floating interest rates, many of those companies that took on debt when rates were ultra low during the pandemic have struggled under high borrowing costs in recent years. Many are now showing signs of pain even as the Federal Reserve brings rates back down.

In the US, default rates on junk loans have soared to decade highs, according to Moody’s data. The prospect of rates staying higher for longer — the Federal Reserve last week signalled a slower pace of easing next year — could keep upward pressure on default rates, say analysts.

Many of these defaults have involved so-called distressed loan exchanges. In such deals, loan terms are changed and maturities extended as a way of enabling a borrower to avoid bankruptcy, but investors are paid back less.

Portfolio managers worry that these higher default rates are the result of changes in the leveraged loan market in recent years.

Despite the rise in defaults, spreads in the high-yield bond market are historically tight, the least since 2007 according to Ice BofA data, in a sign of investors’ appetite for yield.

Still, some fund managers think the spike in default rates will be shortlived, given that Fed rates are now falling. The US central bank cut its benchmark rate this month for the third meeting in a row.

Some analysts blame loosening credit restrictions in loan documentation in recent years for allowing an increase in distressed exchanges that hurt lenders.

This week’s fun finds

The best music written about winter

In C.S. Lewis’s “The Lion, the Witch and the Wardrobe”, Mr Tumnus, a faun, laments that the White Witch has made Narnia “always winter, but never Christmas”—implying that only Christmas makes winter bearable. But the season offers other pleasures: skiing, if you enjoy elaborate dressing rituals; snowshoeing, if walking is not slow and cumbersome enough; or, best of all, staying inside and admiring the gelid landscape through thick windows, with a cup of something steaming. Here’s what to listen to during the short, frosty days and long nights (and not a carol on the list).