The path less travelled

Now live on the website, a new piece: The path less travelled

It’s a look back over the last 15 years and discusses the inflection points we called out over the years. We don’t see these often and believe we’re in one today (which we talk about at the bottom of the piece).

We don’t invest in businesses because of macro thoughts, however we keep macro-level market issues in mind when looking for potential risks or what to avoid. We’ve always done our best to communicate those risks to the likeminded investors willing to join us along the way.

15 years is a long time to cover, so we added a timeline on the PDF’s first page to help you navigate between sections:

.png)

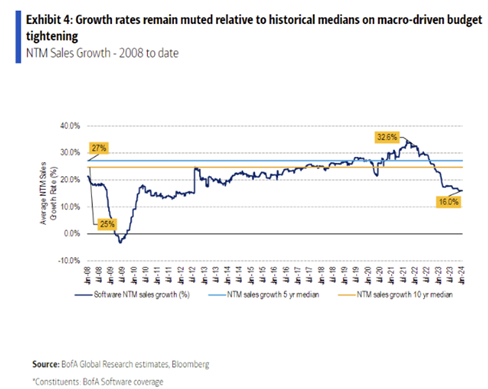

This week in charts

PE distributions

Equities

Correlation

Top 5 by market-cap

Software businesses

Trade

The Six Months That Short-Circuited the Electric-Vehicle Revolution

The Michigan plant where the F-150 Lightning electric truck is built used to vibrate with excitement.

President Biden visited in 2021 and test drove the blazing-fast pickup. Before the first ones even started rolling off the assembly line in the spring of 2022, Ford said it would expand the factory to quadruple the number it could build.

That energy is rapidly fading. Ford is cutting the plant’s output by half, and workers are relocating to other facilities, mostly those making gas-powered pickups and SUVs.

As recently as a year ago, automakers were struggling to meet the hot demand for electric vehicles. In a span of months, though, the dynamic flipped, leaving them hitting the brakes on what for many had been an all-out push toward an electric transformation.

A confluence of factors had led many auto executives to see the potential for a dramatic societal shift to electric cars: government regulations, corporate climate goals, the rise of Chinese EV makers, and Tesla’s stock valuation, which, at roughly $600 billion, still towers over the legacy car companies.

But the push overlooked an important constituency: the consumer.

Last summer, dealers began warning of unsold electric vehicles clogging their lots. Ford, General Motors, Volkswagen and others shifted from frenetic spending on EVs to delaying or downsizing some projects. Dealers who had been begging automakers to ship more EVs faster are now turning them down.

Even Tesla Chief Executive Elon Musk warned of “notably lower” growth in vehicle deliveries for the company in 2024.

“This has been a seismic change in the last six months of last year that will rapidly sort out winners and losers in our industry,” said Ford Chief Executive Jim Farley on an earnings call in early February. EV sales continue to grow, and auto executives say they remain committed to the technology. But many are recalibrating their plans.

Ford has pulled back on EV investment and could delay some vehicle launches, while increasing production of hybrids, which run on both gasoline and electricity. It lost a staggering $4.7 billion last year on its battery-powered car business and projects an even bigger loss this year, in the range of $5 billion to $5.5 billion.

Some auto executives acknowledge they got ahead of the market with overzealous demand projections. Pandemic-era supply-chain shocks and a resulting car shortage created long waiting lists and early buzz for EVs, making the industry overly optimistic.

Only later, as a barrage of new EVs hit the market, did executives realize that car buyers were more discerning than they expected. Many were hesitant to pay a premium for a vehicle that came with compromises.

Farley and other industry CEOs are still confident that EVs will eventually take off, albeit at a slower pace than initially envisioned. But for now, the massive miscalculation has left the industry in a bind, facing a potential glut of EVs and half-empty factories while still having to meet stricter environmental regulations globally.

“Ultimately, we will follow the customer,” GM Chief Executive Mary Barra told analysts this month.

Trouble ahead

Then warning signs began to appear. In mid-January of last year, Tesla slashed prices on some models by more than 20%, triggering a chain reaction.

Used-car dealers who had Tesla Model 3s and Model Ys in stock saw their values plummet by thousands of dollars. Customers who had bought Teslas at higher prices were furious.

“Why cut EV prices when demand is greater than supply?” Bank of America analyst John Murphy wondered.

Musk insisted that there was no demand problem. The company was trying to broaden appeal by making its cars more affordable, he told analysts.

Inside Ford, staffers analyzed what Tesla’s cuts might mean for its own EV sales. About two weeks later, Ford reduced prices on some versions of its Mustang Mach-E SUVs by nearly 9%.

Speaking to analysts in May, Farley largely shrugged off the pricing pressures, saying they weren’t reflective of broader interest in EVs. He remained upbeat about Ford’s outlook, reiterating plans to expand Lightning output.

As car companies entered the summer-selling season, there were other worrying signs. U.S. EV sales for the first half of 2023 rose 50% from a year earlier, down from a 71% increase in the first half of 2022.

The wave of early EV adopters willing to splurge had receded, and the next round of potential customers was proving more hesitant. They had more questions about how far a car could go on a single charge, and the life expectancy of batteries. They worried about charging times, repair costs, and not having enough places to plug in, according to dealers and surveys.

Interest rates were rising, pushing up monthly payments on EVs, which already were selling, on average, for about $14,000 more per vehicle than gas-engine models, according to research firm J.D. Power.

GM was having trouble processing battery cells, a bottleneck that was preventing it from getting EVs to showrooms. Manufacturing delays left buyers waiting for delivery of models such as the Cadillac SUV and Hummer pickup truck.

Late last July, GM’s Barra told analysts plenty of consumers still wanted the company’s EVs. “These vehicles are getting to the dealers’ lots, and if they’re not already sold, they’ve got a list of people who are waiting for them,” she said.

Two days later, Ford’s Farley struck a different tone. “The paradigm has shifted,” he told analysts. Although consumers were still buying EVs, Ford’s pricing power was deteriorating compared with gas-engine models, he said, and the market for EVs would remain volatile.

Jefferies analyst Philippe Houchois asked Farley what had changed. “A few weeks ago when we saw you in Detroit…it’s like you had religion” on EVs, he told the CEO.

Farley replied that Ford was responding to market realities.

Changing plans

The unraveling came swiftly. In a single month last fall, the average interest rate on an electric-car purchase jumped from 4.9% to 7%, making monthly payments even less affordable for some shoppers, said Tyson Jominy, vice president of data and analytics for J.D. Power.

Suddenly, once-long waiting lists for EVs shrank and buyers dropped reservations.

Over a 10-day span in October, the tone of automakers in Detroit and beyond turned gloomier. GM said it would delay by one year a $4 billion overhaul of a suburban Detroit factory to build new electric pickup trucks, citing “evolving EV demand.”

The next day, Elon Musk said that not as many people could afford a Tesla given higher interest rates and tougher economic conditions. Affordability was keeping a lid on demand, he said during a call to discuss third-quarter results.

A week later, on GM’s quarterly call, Barra described the transition to EVs as “bumpy,” and said the company wouldn’t meet a self-imposed goal of producing 400,000 EVs over a two-year period through mid-2024.

Two days later, Ford said it would defer $12 billion in electric-vehicle investments and focus on increasing hybrid production, citing the need to better match demand.

By late last year, it was becoming clear that sales of hybrids—once dismissed by some automakers as an unnecessary half-measure—were taking off and would outsell EVs in 2023.

“People are finally seeing reality,” said Toyota Motor Chairman Akio Toyoda. For years, Toyota and other EV-cautious carmakers had been touting hybrids as a consumer-friendly way to reduce carbon emissions.

In November, thousands of U.S. dealers signed a letter urging Biden to ease proposed regulations that would push the industry to sell more battery-powered cars. “Last year, there was a lot of hope and hype about EVs,” the dealers wrote. “But that enthusiasm has stalled.”

China’s consumers tighten belts even as prices fall

Consumer prices in the world’s second-largest economy have been in deflation for the past four months, falling at their fastest annual rate in 15 years in January. While the headline figure is driven by food and prices are edging higher in other sectors, businesses selling everything from cosmetics to electrical goods are offering discounts. Car prices are falling at their fastest rate in at least 22 years.

The deflation data taps into long-standing concerns over consumer demand as policymakers seek to restore momentum to the world’s second-largest economy. While growth of 5.2 per cent in 2023 benefited from a low base effect the previous year because of the coronavirus pandemic, consumers will need to play a stronger role this year if the economy is to grow again at the same rate.

But with the property market, historically a core driver of confidence, still under pressure, consumer caution has persisted even as people have headed into the Chinese new year, traditionally a period of big spending. Weak price growth is not automatically encouraging people to spend.

“Theoretically low prices should increase purchasing power of consumers, but that hasn’t been the case,” said Louise Loo, lead economist at Oxford Economics. “We think the reason is because the deflationary mindset has been quite entrenched.”

Official data showed retail sales rose 7.4 per cent in December, albeit against a low base in December 2022 when the pandemic swept across the country. Over the full year, affected by similar base effects from lockdowns, retail sales rose 7.2 per cent.

A Morgan Stanley consumer survey for December, published in January, found just over half of respondents expected the economy to improve in the next six months. But it also noted that 76 per cent of consumers have made spending cuts to at least one category in the past six months, and that across all categories, consumers were downgrading to cheaper brands more often than they were upgrading to more expensive ones.

A “lack of income growth” was behind low consumption, suggested Fred Neumann, co-head of Asian Economics at HSBC. The Morgan Stanley survey showed that only 45 per cent of consumers expected household finances to improve over the next six months, the joint-lowest level in the past year.

Auto sales, which rose 12 per cent over 2023, are one sign of lower prices supporting demand, though Loo said the auto data had been “volatile”.

Across major brands in China, genuine falls in prices can be difficult to distinguish from a constant marketing schedule of discounts and deals.

Yaling Jiang, an analyst of consumer markets, said that some price cuts, such as an Apple discount on new phones, were just “regular marketing”. But she added the “premium that Chinese consumers are willing to accept is going down”, in part because savvier domestic buyers had “a higher understanding of the manufacturing process”.

From afar, China Evergrande Group had all the makings of a killer distressed-debt trade: $19 billion in defaulted offshore bonds; $242 billion in assets; and a government that appeared determined to prop up the country’s faltering property market. So US and European hedge funds piled into the debt, envisioning big payouts to juice their returns.

What they got instead over the course of the next two years is a harsh lesson in the dangers of trying to bargain with the Communist Party. The talks are now dead — a Hong Kong court has ordered Evergrande’s liquidation, and the bonds are nearly worthless, trading in secondary markets at just 1 cent on the dollar.

In the aftermath of the Jan. 29 wind-up order, the biggest in China’s history, key players on both sides of the negotiations paint a Kafkaesque picture of endless micro-managing by unidentified government handlers that was communicated to investors through a mind-numbing maze of channels, only to then be interrupted by months-long gaps in dialogue. The last of those gaps came — to the shock of creditors — after the court’s December ruling giving the two sides one final chance to cut a deal.

While global money managers have long known that the Chinese government exerts influence over corporate affairs in ways that are uncommon across the developed world, Evergrande was nonetheless a first-hand education for many of them in just how much authorities will intervene for the sake of political and economic expediency.

The 1-cent-on-the-dollar price on the bonds, they say, sends a warning to investors as other Chinese companies, including Country Garden Holdings Co., follow Evergrande into default amid an economic slump that officials have struggled to fix. And the country’s disregard for foreign creditors almost certainly means more of them will get sold for parts.

Of course, it’s more than just Beijing’s involvement that caused Evergrande’s bonds to crater. The nation’s deepening property-market slump, a $7 trillion stock rout and a tepid policy response are all weighing on broader sentiment. The fact that the bulk of the company’s assets are either already seized or located not in Hong Kong but mainland China — potentially out of reach of bondholders including Davidson Kempner Capital Management, King Street Capital Management and Contrarian Capital Management, has also contributed to rock-bottom recovery expectations.

Soon after the company’s 2021 default, a risk-management committee dominated by officials from Evergrande’s home province of Guangdong — in part made up of company executives and state-affiliated debt managers — was formed to guide the overhaul. Provincial authorities also said that year that they would send a working group to strengthen internal controls and management of Evergrande.

Over the course of the negotiations, Evergrande representatives would sometimes refer to “Guangzhou” (the capital of Guangdong province) as responsible for vetting virtually all key decisions, yet it remained unclear to creditors which combination of entities or individuals they were alluding to.

Investors and advisers lamented not being fully aware of whose interests were being prioritized in negotiations, nor which layers of government they were dealing with.

The secretive yet omnipresent group never directly interacted with those involved in offshore debt talks, said the people familiar. Their views were relayed to the company’s financial advisers, China International Capital Corp. and Bank of China International Holdings, which would then pass information on to bondholders via a convoluted web of communications that consisted of lawyers and advisers both in Hong Kong and the mainland, the people said.

The group could, and did, veto creditor proposals with minimal explanation, the people added.

In one example, it balked at an early offer that would’ve given offshore creditors access to the future income streams generated from Evergrande’s onshore projects. That cash instead was to be preserved for ensuring the delivery of other company projects, the people said. That reasoning wasn’t communicated to investors, who were only told the terms were not acceptable, they added.

Still, early last year, Evergrande and its creditors were seemingly near an agreement to overhaul the company’s offshore debt load. Its $4.7 billion of dollar bonds due 2025 spiked as high as 11 cents.

But a series of setbacks, including weaker than expected property sales, push back from regulators and the detention of Evergrande billionaire chairman Hui Ka Yan, ultimately torpedoed a deal, fueling further frustration and leading to a significant breakdown in talks, the people said.

In early December, when a Hong Kong court gave Evergrande one last chance to strike a deal, the company’s representatives largely fell silent. Over a month went by before they finally contacted the offshore creditor group again — via email.

When they did, their proposal shocked bondholders. Not only did it do little to strengthen their offer, it crossed a number of red lines the creditor group thought were clearly laid out, people with knowledge of the situation said.

One key sticking point was the claims of a group of creditors identified as class C, which consists of some state-run banks, according to the people.

While Evergrande eventually agreed to give creditors controlling stakes in two offshore listed units’ equity — a compromise it previously refused to make, the plan would have put the foreign bondholder claims and the debt held by the banks on equal footing, shrinking the pie for the international investors, multiple people familiar said. Offshore bondholders deemed the plan particularly objectionable because class C creditors also have access to onshore assets that they have little recourse to.

A counteroffer was quickly made, and the company sent over another proposal on Jan. 29, just hours before the latest scheduled wind-up hearing.

In the end, the judge overseeing the case, frustrated by the lack of progress on a deal, ordered the company’s liquidation.

‘Serious Setback’

The company’s court-ordered liquidators from Alvarez & Marsal now begin the process of seizing and carving up the developer’s 1.74 trillion yuan ($242 billion) of assets, more than 90% of which are located in mainland China. Yet given Hong Kong’s insolvency proceedings have limited recognition in China, creditors face an uphill battle recouping losses.

“Authorities are not likely to allow offshore claimants to secure valuable onshore assets while effectively insolvent developers struggle to meet politically tense onshore obligations,” said Brock Silvers, managing director at private equity firm Kaiyuan Capital. “This is a serious setback for China’s still-developing credit markets and can only exacerbate declining market sentiment as foreign capital increasingly seeks lower risk outlets.”

This week’s fun finds

AI is shaking up online dating with chatbots that are ‘flirty but not too flirty’

As of Valentine’s Day 2024, the world of online romance looks very different. An increasing number of people are using artificial intelligence to flirt, whether that means generating messages for dating apps, uploading profiles, or evaluating compatibility with a “situationship.”

In the U.S., 1 in 3 men ages 18 to 34 use ChatGPT for relationship advice, compared with 14% of women in the same age range, according to a survey last month on AI platform Pollfish. Startups focused on AI-generated messages for dating are seeing booming demand. A Russian man who programmed a chatbot to converse with more than 5,000 women on Tinder is now engaged to one of them.

The phenomenon even found its way last year into an episode of Comedy Central’s “South Park,” when the character Stan Marsh asked another character, Clyde Donovan, for advice on responding to his girlfriend’s texts.

“ChatGPT, dude,” Clyde told Stan, in the school hallway. “There’s a bunch of apps and programs you can subscribe to that use OpenAI to do all your writing for you. People use them to write poems, write job applications. But what they’re really good for is dealing with chicks.”

Some form of generative AI has entered virtually every industry, from financial services to biomedical research. Nvidia, the leading provider of processors used to power most generative AI models, has seen its revenue soar, and its market cap now rivals that of Amazon. OpenAI has emerged as one of the hottest startups on the planet, thanks to its large language models (LLMs), while Anthropic, founded by former OpenAI employees, is trying to catch up.

Generative AI for dating may sound bleak, but it’s not necessarily surprising. Booming interest in the sector has set the stage for a rush of investments and a mountain of new products and services, including some targeting online romance.

YourMove.AI, an AI dating tool that offers a range of services such as drafting messages, analyzing conversations and evaluating users’ dating app profiles, has about 250,000 users, founder Dmitri Mirakyan estimates. Launched in 2022, YourMove receives about 200,000 site visits per month, he said, and revenue has grown roughly 20% month over month.

“The types of people that use this – you’d think it’s mostly just people that feel awkward, but there’s a ton of people who are just introverts,” Mirakyan told CNBC. He said users include people who are shy, speak English as a second language, are navigating cultural change or are simply newbies to online dating.

A ChatGPT user in New York told CNBC that he decided to use OpenAI’s service to draft messages to women on dating apps after the “South Park” episode last March. He would plug in a woman’s opening message to ChatGPT and prompt it to act like a single person with the goal of getting a date. He made sure to tell the chatbot not to ask the person out immediately.