Even though there are still travel restrictions, doesn’t mean the Investment team’s latest reading and listening recommendations can’t help you escape some of the summer heat.

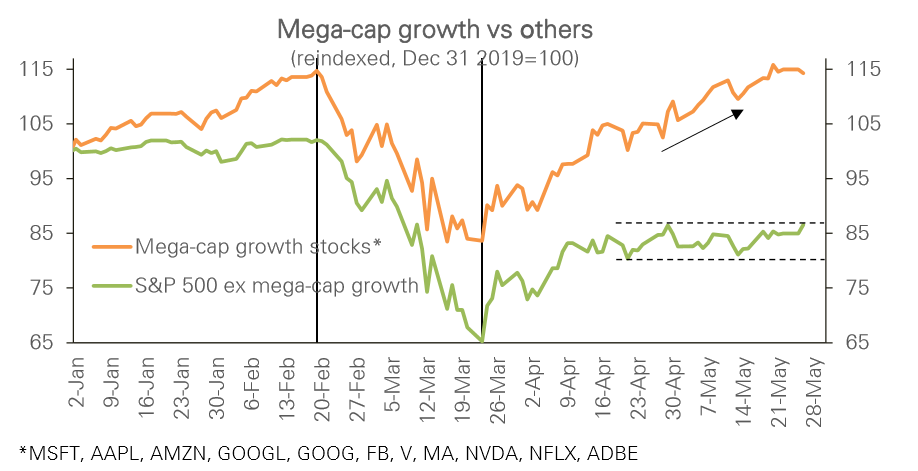

We guess this makes sense when Apple, Amazon, Microsoft and Google combined are now worth more than the entirety of the Japanese stock market.

“Can ‘bad’ things happen to an otherwise ‘good’ investment portfolio? To answer this question, I looked at the performance of a very large and well-known investment portfolio that has a long history of exceptional results. This particular portfolio provides a good ‘test case’ because its history goes back more than 50 years. Therefore, its success clearly cannot be attributed to mere luck.”

Over its lengthy tenure the portfolio has widely outperformed its benchmark, adding significant value for investors over time. However, all sorts of bad things happened to this portfolio all along the way:

- There were 11 calendar years over its tenure, where this ‘good’ portfolio would have lost you money. To add insult to injury, in seven of those negative years the portfolio also underperformed its benchmark.

- There were 17 years in total where the portfolio underperformed its benchmark. That’s almost 1/3rd of the time.

- There were 21 years where this otherwise ‘good’ portfolio experienced a calendar year return that was negative and/ or worse than its benchmark.

- There were 20 calendar years where the portfolio returned less than 10%.

- And finally, it also experienced a couple of prolonged periods of particularly poor results. Throughout its history this portfolio experienced two separate periods of time where it had either a negative rate of return and/or underperformed its benchmark for four years in a row. In other words, if you had hired this particular portfolio manager at the start of either of these periods, and looked back at your results four years later, you would have experienced either negative or relative underperformance in each and every one of the previous four years.

In either of these scenarios, many investors would have promptly pulled their money and fired the manager! The “portfolio” we’ve analyzed above is none other than that of Berkshire Hathaway, and the ‘portfolio manager’ you’d have fired would have been the world’s greatest investor himself – Mr. Warren Buffett!

Over the 54 year period from the beginning of 1965 to the end of 2018, Buffett/ Berkshire returned an average of 20.5% per year, more than doubling the S&P500 Index, returned 9.7% per year over the same period

Truly bad things can only happen to good investment portfolios through our own behaviour; i.e. how we react to “bad” events such as temporary underperformance. If the portfolio itself is indeed a ‘good’ one by definition, it won’t do bad things to you. Only you can do bad things with it.

Retail sales

Topline retail activity is now just -0.8% away from the pre-pandemic level.

There is wide dispersion within the sectors and the “work-from-home” theme is clearly visible when we look at the fact that groceries are 11.5% above pre-Covid, e-tailing is sitting at 20.9% higher and now sporting goods etc. has ramped up to 23.1% above the pre-pandemic level.

Household spending

Although average spending fell for all households as the economy shut down at the start of the pandemic, unemployed households actually increased their spending beyond pre-unemployment levels once they began receiving benefits.

Store openings and closures in the US