First quarter commentaries are now live!

This quarter, George Droulias discusses the three key levers that we believe drive a business’ worth, while Frank Mullen talks about the importance of remaining disciplined when managing credit in the face of market exuberance.

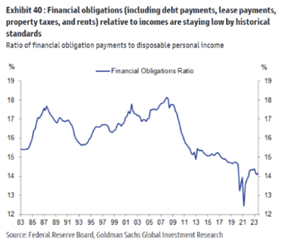

This week in charts

China

Gold

Capital Expenditures (CapEx)

Employment

Private equity

LBO loans

A $10 Billion Copper Mine Is Now Sitting Idle in the Jungle

When the group of mining executives arrived at Panama’s regal Palacio de las Garzas, they were ushered past the ornate, wood-paneled ceremonial rooms and straight to the private office of the president.

This was December 2016, before the upswell of anti-mining protests that would throw the country into chaos, and the team from First Quantum Minerals Ltd. were greeted as old friends. After all, they were building the country’s most important project since the Panama Canal had been opened a century earlier.

But as they compared notes on the progress of their Cobre Panama copper mine, the president issued a warning.

First Quantum had lucked into an unusually sweet deal in Panama, he said. Sooner or later, the company would have to agree on new terms with the government and pay more taxes. What was left unsaid: it would be better to do it sooner, under a business-friendly government like his, than to gamble on Panamanian politics.

The stakes were high. The mine was set to be the centerpiece of Panama’s economy, generating between 4% and 5% of its gross domestic product and employing one in every 50 workers in the country. For First Quantum, which had borrowed heavily to construct a mine in the dense Panamanian jungle, it simply had to succeed.

Philip Pascall was unmoved. A swashbuckling Zimbabwean who had built First Quantum from scratch by making bold bets that few others had the stomach for, he brushed aside the president’s warning and quickly moved the conversation away from tax.

It was a gamble that would prove disastrous. Today, the $10 billion mine is sitting idle, shuttered by nationwide protests over a new tax deal signed in October. First Quantum’s share price has plunged by roughly half, and the company is being circled by predatory rivals.

This account of how First Quantum's flagship investment fell apart is based on interviews with more than a dozen people involved in the project over a decade.

It is in part a tale of First Quantum’s hubris, as the company’s bosses sought to build the mine fast and keep costs low, despite unsettled tax disputes and legal issues. Pascall dismissed private warnings not only from Panama’s government but also from his own advisors that the tax deal put his company in a vulnerable position.

But it is also a story that resonates far beyond the walls of First Quantum’s offices and the borders of Panama, highlighting a dilemma at the heart of the global transition away from fossil fuels. While governments are pushing to secure the raw materials to build electric vehicles, solar panels and high-voltage cables required for the energy transition, few of their citizens want the mines needed to produce them.

The fate of Cobre Panama is one of the central questions facing the miners, traders and hedge fund managers who have gathered in Santiago in Chile for the copper industry’s annual Cesco Week event.

“If I was a copper mining company looking at Latin America, would I want to sink a 50-year operation into one of these countries where there is this rising risk?” said Gracelin Baskaran, a research director and senior fellow for the Energy Security and Climate Change Program at the Center for Strategic and International Studies.

“If the sector is risk-averse, they don’t invest. And if they don’t invest, we don’t have what we need for an energy transition.”

Charismatic Leader

Trailblazing projects like Cobre Panama have long been a hallmark of First Quantum’s business. Headquartered in Canada, the company was founded in 1996 by Philip Pascall and his brother Matt.

The brothers developed copper mines in countries like Zambia and the Democratic Republic of the Congo, regions with low investment grades where few of its competitors dared to venture. While mines can often take decades to build, the Pascalls cultivated a reputation for getting their projects done ahead of schedule.

In a rare interview in 2013, Philip Pascall described the ethos of his firm to The Australian: “We dare where others don’t, we try new things out, learn from our experiences and have earned a reputation for delivering not only to budget, but before schedule in an industry prone to overrunning both.”

Their boldness was rewarded in the 2000s, as demand from China supercharged the price of copper. By the early 2010s, First Quantum had become a multibillion-dollar success story. With cash to spend and growing ambitions, Philip set his sights on a deposit in Panama, a country until then little touched by the mining industry.

The firm launched a $5.5 billion takeover of the deposit’s owner, Inmet Mining Corp., that quickly turned hostile after the smaller firm twice rejected First Quantum’s approaches.

The end result was a $10 billion mining complex larger than the size of San Francisco, isolated in Panama’s tropical rainforest, and capable of producing more than 350,000 tons of copper in a year — enough to build about five million electric vehicles. In an industry where many of the largest deposits have been depleting for decades, it was a rare example of a major new mine.

And the timing seemed fortuitous. China’s industrialization was being supplanted as the major driver of projected copper demand by a new juggernaut — the energy transition. The electric vehicles, charging stations and high-voltage cables needed to electrify the world’s transportation will all require lots of copper. Mining executives started talking about the gap between the amount of copper that would be needed to reach net zero and the anticipated supply from the world’s existing mines. The world would need dozens of new copper mines, they said.

First Ore

First Quantum’s success had much to do with its leader, Philip Pascall, and rapport he forged with Juan Carlos Varela, Panama’s president from 2014 to 2019. The two men would dine together, with Philip sometimes supplying wine from his brother’s vineyard in Cape Town.

Varela was eager to see Cobre Panama built. He kept a piece of the first ore rock mined from Cobre Panama in his office. The night before the mine opened in 2019, he joined First Quantum staffers at a luxury resort on Panama’s southern coast to dine on sushi and toast the project’s completion.

Still, the honeymoon wouldn’t last. Even before Varela left office in 2019, Cobre Panama faced increasing scrutiny. The project’s tax requirements were enshrined in an outdated contract struck in 1997 — a time of record-low copper prices — long before the deposit’s value was fully realized. The details of the contract, which First Quantum inherited from the concession’s previous owners, required the miner to pay a 2% royalty rate on minerals revenue — a sweet deal for a metals producer.

Pascall had ignored Varela’s admonitions about the tax deal. In the years before Cobre Panama opened, both Varela and a former Supreme Court justice and board member for the mine’s local subsidiary had pressed Pascall to start arranging a contract that would satisfy the country’s higher tax demands. Insiders at the company said First Quantum’s leadership never acquiesced to Varela’s demands, but Varela didn’t force the issue either, instead allowing First Quantum to proceed with a lenient tax arrangement.

The tax benefits became hard to ignore once the mine opened. In 2019, Cobre Panama’s first full year of operation, the mine's royalty payments to Panama were a sixth of what First Quantum paid to Zambia for its Kansanshi mine. (In that period, though, Zambia's tax rate was notably high for foreign mining firms).

The disparities were enough to draw the ire of a new government. When Varela’s business-friendly administration was replaced by the centre-left party of Laurentino Cortizo, the new administration moved to secure a better tax deal for the country.

Cortizo didn’t maintain the same friendly relations with First Quantum. He had steered Panama through a cataclysmic recession caused by the Covid pandemic, that saw employment fall drastically and inflation spike while container ships sat idle in the Panama Canal. Now he needed to refill the government’s coffers, and First Quantum, the country’s biggest investor, became an obvious target.

The government pushed for significantly higher royalties as well as a minimum annual flat tax of $375 million. When the company pushed back, Panama threatened to shutter the mine altogether.

“They were tough negotiations,” said Robert Harding, First Quantum’s chairman. “We were trying to protect our interests and they were trying to protect theirs.”

After long delays and standoffs and over four years of negotiations, the government and company reached a tentative agreement in March last year. First Quantum acquiesced to the bulk of Panama’s demands in exchange for a 20-year extension on the mine’s operating contract.

Hostility Brews

To the outside world, it looked like the crisis had been averted. Months passed in relative calm, and the mine kept churning out huge amounts of copper.

Yet on the ground, hostility was brewing. Panama was already seething with discontent over inflation, high unemployment and corruption, and there was long-standing resentment over Cobre Panama’s environmental impact and its contribution to the economy. With a national election looming, the mine became a focal point for all the country’s ills.

In October, when Panama’s congress approved the new contract with First Quantum in what should have been a formality, the decision fueled an uprising of protests that paralyzed large swathes of the country.

One of the driving forces behind the opposition was a powerful and confrontational construction union called Suntracs, which has a history of clashing with companies operating in Panama. The group had sought early on to take part in the mine’s construction, and Suntracs members subsequently stormed the gates of the mine and assaulted employees at least three times between 2015 and 2018. Now Suntracs played a key role in stirring up protests and pushing labor issues to the forefront.

Across the country, protesters blockaded highways and rallied in the cities. Local boats, some of them operated by Suntracs, blocked access to Cobre Panama's coastal port for weeks, preventing First Quantum and its suppliers’ ships from docking.

As the civil unrest raged, First Quantum had largely lost touch with the government’s decision making, according to employees who spoke with Bloomberg News. The close-knit relationship Philip had once maintained with Varela was virtually absent between Cortizo and Philip’s son Tristan, who had taken over from his father as CEO after overseeing Cobre Panama's construction as the project's general manager.

When Cortizo called for a national referendum on the mine’s operating contract in October — a short-lived idea meant to calm mass demonstrations — Tristan Pascall and First Quantum’s other top executives were provided no advance notice. The soft-spoken executive largely conducted damage-control from the company’s London office, eventually visiting Panama briefly in late November following Cortizo’s call to shutter the mine. But Panama’s course was set. The mine produced its last ton of copper in November and has been sitting idle ever since.

Cautionary Tale

For the wider mining industry, the story of First Quantum in Panama has become a cautionary tale.

“It’s just a reminder that it’s so, so important that there’s mutual trust, and that what we’re doing is in the interest of all constituents,” said Jakob Stausholm, Chief Executive Officer of Rio Tinto, whose predecessor was ousted after the company irreparably damaged an ancient Indigenous heritage site in Australia. “You cannot run the risk of turning a blind eye to that side of the business.”

In Panama, First Quantum has embarked on a media blitz ahead of presidential elections in May, hoping that it can gain enough popular support to persuade the next government to allow the mine to restart. The company says it’s spending $15 million to $20 million per month to preserve the site, and has committed to reforesting more than 11,000 hectares of Panama’s rainforest — double the area impacted by mining.

Yet some analysts have predicted the shutdown could last a year or longer, while a question mark hangs over who will ultimately own the mine. The project has attracted interest from the likes of Barrick Gold Corp., a much larger mining firm that boasts a history of dealmaking in challenging jurisdictions.

Cobre Panama’s closure was one of the key catalysts behind a global shortage of copper ore currently gripping the industry, which in turn has drawn bullish investors into the market and helped pushed metal prices to the highest point in nearly two years. The mine accounted for roughly 1.5% of the world’s supply of copper.

And the closure of Cobre Panama has intensified warnings from the mining industry that future supplies of metals like copper may not be sufficient to meet the needs of the energy transition. The International Energy Agency has predicted that by 2030, mines in production or currently under construction will only meet half of global demand for battery metals like lithium and cobalt. Copper mines, meanwhile, are projected to meet 80% of global demand in that same time frame.

The operation is “only one example of the geopolitical climate within which today’s copper and other commodity mining operations exist,” said Andrew Kireta Jr., president and CEO of the Copper Development Association, a US-based industry group.

“If we proceed with a business-as-usual approach, these supply constraints and others will impact the US’s ability to meet the projected steep demand acceleration for copper to build out clean energy infrastructure and transition to electric vehicles.”

US FTC preparing to sue to block $8.5 bln takeover of Capri by Tapestry, NYT Dealbook reports

The deal, which would bring together top luxury labels such as Tapestry's Kate Spade, Stuart Weitzman and Capri's Jimmy Choo and Versace, received regulatory clearance from the European Union and Japan on Monday.

The FTC's five commissioners are expected to meet this week to discuss the case, a move that could precede a formal vote on whether to file a lawsuit, according to the report.

The merger aimed to create a U.S. fashion powerhouse to compete better with bigger European rivals amid a slowdown in luxury spending.

This week’s fun finds

Our internal hot sauce challenge club received a hot tip this week to test The End. Flatline hot sauce followed by Stingin’ Hotter Honey, Red Lava edition. The End left everyone thinking “What did we ever do to you?”

Before

Reviews:

- “Why is it black?”

- “It tastes like burning rubber smells”

- "Are you crying?"

{kind=link}