This week in charts

Spreads

Interest payments

Gold

Fixed income

Used vehicles

Battery manufacturing

Cyber attacks

Maturities

Real returns

Lost in space

Downtown Toronto’s largest office landlords are plagued by a growing problem: too many empty floors.

But all buildings are not equal, and a new analysis pulls back the curtain on what’s going on behind the shimmering glass of all those skyscrapers that define the city’s skyline, revealing a deeply divided office market.

While some towers are chock-full of tenants, one-third of the biggest office buildings in the core of Canada’s most important financial district are at least one-fifth empty, with some grappling with even larger voids of up to 50 per cent.

The characteristics of the fullest buildings provide insight into how landlords are navigating the new world of remote work at a time of high interest rates and a stalling economy.

It all raises questions about what might happen to valuations in Toronto’s office market if so much floor space remains left unfilled and what the effects on surrounding businesses will be. With some of Canada’s largest pension funds prominent landlords in the Toronto market, the implications go far beyond the power corner of King Street and Bay Street.

“Prior to the pandemic, downtown Toronto was a landlord’s market with very low vacancy and availability and since the pandemic it’s moved towards much more of a tenant’s market,” said Carl Gomez, chief economist and head of market analytics at CoStar, a Washington-based commercial real estate information provider that has operated in Canada since 2014.

Today, Toronto is one of the few Canadian cities where office vacancies are still on the rise. The percentage of space available to lease in the financial district was 17 per cent as of late April, according to CoStar, higher than the city as well as the rest of the country.

One thing is clear: It’s a tenant’s market.

No longer can landlords profit simply from owning an office tower in Canada’s financial capital. Nor is easy access to the city’s underground path and public transportation enough to attract tenants. Owners have put in fancy showers, some have Dyson hairdryers, while others are providing activities such as trivia in the afternoon to entice tenants to love their office life once more.

As the CoStar data show, the impact of the pandemic on Toronto’s office towers has not been even, with some towers seeing availability rates rise sharply while others have fared much better.

The most common explanation is that tenants are abandoning lower-class buildings to move into higher-rated towers with more amenities such as green spaces and cutting-edge ventilation systems, ditching Class C for Class A towers.

Retailers near emptier buildings in the financial district aren’t so fortunate.

The return of foot traffic to downtown appears stalled. The share of employees in Toronto’s financial core has been stuck at about 60 per cent of prepandemic occupancy since early February, according to consulting group Strategic Regional Research Alliance. The peak day is Wednesday at 70 per cent and the lowest is Friday at 37 per cent.

Businesses have marvelled at how easy it is to find space in coveted buildings. Accounting and business advisory firm MNP LLP said it got a prime location at a 30-per-cent discount to prepandemic days. CIRO, the investment watchdog, said it had a number of properties to choose from.

A flood of new office space has come onto the market in recent years. Since the start of the pandemic, 11 downtown office towers have opened including the 49-storey CIBC Square and the 47-storey TD Terrace.

The new skyscrapers have increased the amount of office space in the core by 7.8 million square feet, or 9 per cent, according to Altus, a commercial real estate consulting firm. That occurred as demand dropped dramatically and tenants tried to get rid of their space on the sublet market.

Over the next two years, three more office towers will open in the financial district, including CIBC Square’s second 49-storey tower. The new additions will increase office space by another 2.5 million square feet, or 2.8 per cent, according to Altus.

As tenants move into their new offices at places like TD Terrace and CIBC Square, they are leaving their former landlords with space to fill.

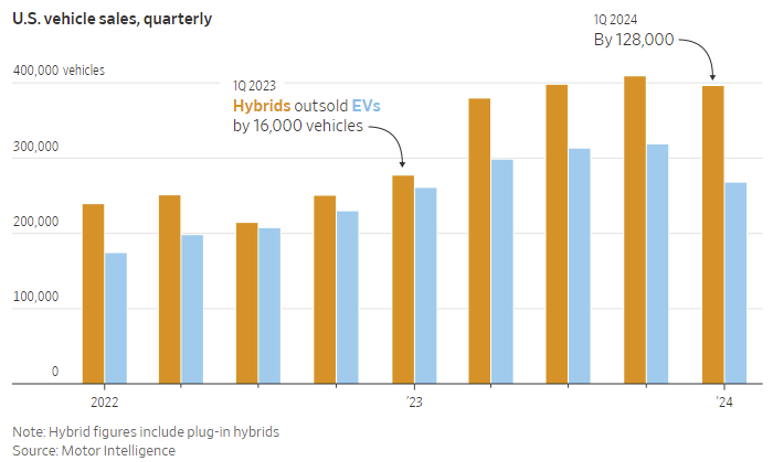

Carmakers bet on hybrids as shift to EVs slows

Global carmakers are stepping up their investment in hybrid technologies as consumers’ growing wariness over fully electric vehicles forces the industry to rapidly shift gear, according to top executives.

A combination of still high interest rates and concern over inadequate charging infrastructure has chilled buyers’ enthusiasm for fully electric cars, prompting a rebound in sales of hybrid vehicles that most of the industry had long regarded as nothing more than a stop-gap.

Tapping the resurgent demand for hybrids was a priority, executives from General Motors, Nissan, Hyundai, Volkswagen and Ford told the Financial Times’ Future of the Car Summit this week.

“We have to invest heavily in the future of plug-in hybrids,” said Mark Reuss, the president of General Motors. “We have to be agile. We have a global tool chest of technical things that we can deploy fairly rapidly.”

The view was echoed by José Muñoz, global president of Hyundai, which is now considering manufacturing hybrids at its new $7.6bn plant in Georgia given more drivers are baulking over buying fully electric vehicles.

“If you asked me six months ago, definitely a year ago, I would have told you . . . fully electric,” said Muñoz. “A lot of things have happened between then and now. Electric is still the future. But now we are seeing a longer transition.”

Electric car sales growth slowed in the US and Europe last year, prompting carmakers to offer discounts. Industry executives have already acknowledged that the market has lost some momentum as future sales growth increasingly depends on demand from mainstream buyers rather than early adopters.

At the same time, there are concerns over whether governments might backtrack on previous plans to force a rapid transition away from petrol-based cars.

Ford’s European boss Martin Sander said that the pace of the transition in Europe was “down to the consumer”, and that US group was prepared to continue selling hybrid models into the next decade.

“We want to make sure that we are setting up our business model so that we are flexible enough” to address shifts in demand, Sander told the summit. “Our whole business and life cycle planning is much more dynamic now.”

US rival General Motors, which had largely eliminated plug-in hybrids from its range, said in January that it would reintroduce the technology.

Consumers’ increasing hesitation comes just as carmakers face a growing threat from Chinese manufacturers rolling out cheaper electric vehicles both in their domestic market and, increasingly, in Europe.

To remain competitive in China, Peugeot needs to stay “agile” to avoid getting sucked into the country’s price war, said its chief executive Linda Jackson. “We’re holding on but the Chinese market is the biggest automotive market in the world so it’s very difficult for a global manufacturer not to be present,” Jackson said.

According to Schmidt Automotive Research, Chinese brands like BYD as well as brands such as Polestar that manufacture in China accounted for almost 10 per cent of the fully electric cars registered in western Europe in March. That is up from just over 4 per cent two years ago.

“We see an increase of competition coming from China brands and other technology worlds,” Nissan’s chief executive Makoto Uchida told the summit.

The threat from Chinese companies has only heightened carmakers’ focus on hybrids, which typically have double-digit margins compared with often lossmaking fully electric vehicles.

For many carmakers, the slower switch is allowing them to continue to squeeze profits from traditional engines while also providing more financial firepower to develop electric vehicle technology.

The majority of the industry still believes that developing profitable fully electric cars is the most important long-term goal.

Earlier this week, Toyota, the biggest champion of hybrids in recent years, said that it planned to lift spending on new technologies by more than 40 per cent after hybrid sales drove the group’s profits to a record last year.

This week’s fun finds

Sushi Friday!

Our partner Nic from Montreal treated the Toronto office today with Sushi Burritos. He gained extra points for originality and delivering lunch 2 minutes before noon. Well done!

Maybe the Italians Were On To Something: Espresso Dose

Why, if the Italian standard (one still written about in books to this day) is 14g for the double dose, would you use 4.5g more coffee for a double shot?