This week in charts

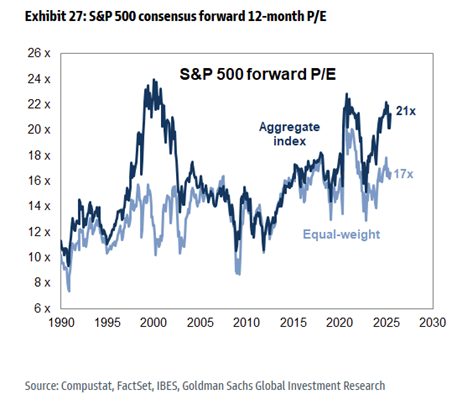

S&P 500 Index valuations vs. their historical average

U.S. vs. global equity price returns

U.S. stock market value relative to GDP

U.S. value stocks vs. growth stocks

Japanese share buybacks

EV/EBITDA since 2005

European equities cash deployment

Corporate bond spreads

U.S. bond and equity correlation

U.S. Aggregate bond index duration vs. High Yield corporate bond duration

Automotive sales by region

As Companies Abandon Climate Pledges, Is There a Silver Lining?

Peter Ford has seen the promise—and the pitfalls—of corporate climate pledges up close. The 40-year-old Briton recently spent five years at Hennes & Mauritz AB trying to cut emissions from the Swedish fashion giant’s vast supply chain, from Cambodian sewing lines to Vietnamese dye houses. He met with hundreds of suppliers, pushed for energy efficiency upgrades and urged the elimination of coal boilers. And to its credit, H&M invested about $200 million a year in these efforts and recently reported a 24% cut in its supply chain emissions.

But Ford isn’t celebrating. “As an industry, it’s not working out yet,” he says bluntly. Apparel emissions are still growing—and could expand an additional 30% this decade, according to McKinsey & Co. While a few brands are doing a lot of work, Ford says, most of the industry “would much rather sit there and wait for things to happen.” That mismatch isn’t unique to fashion. From airlines to banks to retailers, the story is the same: Over the past few decades, more than 4,000 companies have made big climate pledges, but results are scant, and emissions continue to rise.

Worse, we’re now seeing a retreat. In the past year companies around the world have been canceling their climate commitments, some only a few years old. BP Plc is pulling back on renewables and drilling more oil. Coca-Cola Co. and PepsiCo Inc. abandoned or weakened promises they made in 2021 to slash their use of new plastics. Big banks such as Wells Fargo & Co. and HSBC Holdings Plc walked back various plans to reduce their emissions. Walmart Inc. admits it’s behind on its climate targets, while FedEx Corp. says it will likely miss its goal to go electric on half of its delivery truck purchases by 2025. This corporate retrenchment has been particularly acute in the US, where the Trump administration has been busy rolling back climate regulations and withdrawing from international treaties such as the Paris Agreement.

It’s a troubling trend for anyone who prefers life on a hospitable planet. We’re currently on pace to add about 3C (5.5F) of warming this century, which is expected to throw the planet into turmoil with diminished food supplies, wiped-out marine life, brutal heat waves and crippling droughts. But even with those grim prospects, some experts argue that this corporate backpedaling might come with a silver lining. That’s because it could force investors, lawmakers, academics and the broader public to reckon with the fact that voluntary corporate action was never going to stave off climate disaster. This could bring sharper attention to corporate political activities, where even self-proclaimed responsible businesses obstruct regulations needed to phase out fossil fuels and boost clean alternatives.

For years companies have suggested their pursuit of sustainability would naturally follow their quest for profits. Walmart framed its eco-pivot in 2005 as a way to reduce waste, cut costs and promote goodwill. PepsiCo’s then-chief executive officer, Indra Nooyi, put it more elegantly a few years later, when she said using less water and energy isn’t corporate benevolence but rather a way to lower your bills and fatten your margins.

There’s an element of truth to this: Some climate-friendly endeavors, including swapping out lightbulbs and putting up solar panels, quickly pay for themselves and enhance the bottom line. But most projects required to achieve deep decarbonization, such as decommissioning coal boilers or using cleaner fuels, cost gobs of money, and no one knows when or if they’ll ever be cheaper than their dirtier alternatives. As long as these measures remain voluntary, they won’t happen at anywhere near the scale or pace that’s needed. And companies will be free to renege on their promises.

Unfortunately, most companies have talked a big game on climate while working to block or water down the very policies that could drive real progress. Take the US airline industry. Despite skyrocketing emissions, most carriers have vowed to eliminate their planet-warming pollution by 2050. A key part of the plan is to use vastly more sustainable aviation fuel. But this currently accounts for about 0.3% of their total fuel use. Airlines are quick to point out that cleaner fuels cost about two or three times more than conventional jet fuel, and they can’t boost these purchases without putting themselves at a disadvantage to others that keep using cheaper, dirtier fuels.

This, of course, highlights the need for regulation to make sure first movers aren’t punished in the market. In Europe, regulators have stepped in, mandating 2% cleaner fuel now and 6% by 2030. But US carriers vigorously oppose rules like these, including a recent California proposal that would have regulated jet fuel for flights in the state. After airlines questioned the state’s authority to set such rules, California backed off and instead joined the companies to cheer a toothless “voluntary and nonbinding” agreement to increase the use of cleaner fuels.

When asked about these glaring misalignments, companies frequently argue that they rely on trade groups to advocate on a wide range of issues, such as taxation and trade, and that they don’t always agree on every position. This claim doesn’t pass muster with Bill Weihl, who says he used to make the same argument back when he ran sustainability efforts for Facebook. “It’s a weak excuse,” says Weihl, who has since launched ClimateVoice, a nonprofit that pushes companies to support climate policies. “They’re choosing to kick the can down the road so they can get lower taxes and deregulation.”

When it comes to policy positions, who’s putting their money where their mouth is? Advocates point to packaged-goods maker Unilever Plc as one of the rare companies moving in the right direction by regularly examining the climate work of trade groups to which it belongs. In its most recent review, from April, Unilever found that eight of 26 groups were misaligned with its views on climate policy—including the Confederation of Indian Industry, which has pushed for lower petrol taxes and more energy from gasified coal. Importantly, the report also spells out the steps Unilever plans to take to address this misalignment, including potentially leaving groups that continue to obstruct climate action. Any company claiming to be serious about climate should follow Unilever’s lead with this kind of rigorous examination and public reporting.

Clearly regulations are the most effective way to shift this mindset and force companies to pour money into much-needed climate projects. Businesses, however, have gone mute as President Donald Trump wades into their industries to annihilate various climate rules, which will pour billions of extra tons of planet-warming gases into the atmosphere. But there are other ways to pressure a company into speaking up and doing the right thing, including rallying its often large numbers of employees who feel strongly about leaving a livable planet for their children.

This week’s fun find

Mysteriously Perfect Sphere Spotted in Space by Astronomers

Our Milky Way galaxy is home to some extremely weird things, but a new discovery has astronomers truly baffled.

In data collected by a powerful radio telescope, astronomers have found what appears to be a perfectly spherical bubble. We know more or less what it is – it's the ball of expanding material ejected by an exploding star, a supernova remnant – but how it came to be is more of a puzzle.